![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/sp_en_8.gif)

HOW TO CREATE A SLUSH FUND!!!!

I want to

apologize up front for the length of this article but because of Chairman

LaRochelle insisting I do not have correct information; I am forced to provide

proof utilizing town documents. I

would like to think my word is good enough but the town council tries to down

play everything I present to the council.

A representative of the town attended the State of Maine

auction for vehicles and obtained three trucks on various dates. I want to discuss two of these trucks and how

they were obtained. The first one is a

2003 Ford F250 for Public Works. The

cost of the vehicle was $5,500.00. Below

is a copy of the Purchase order with the account the funds were taken

from. If you look at the account

E03-305-5390 you will find it is assigned to the Public Works Department for

Supplies Parts. I have included a copy

of the budget provide by the Finance Director.

This line item is supposed to be used for “provides parts for all units

as necessary”. I cannot believe a Ford F250 truck

qualifies as parts for all units as necessary.

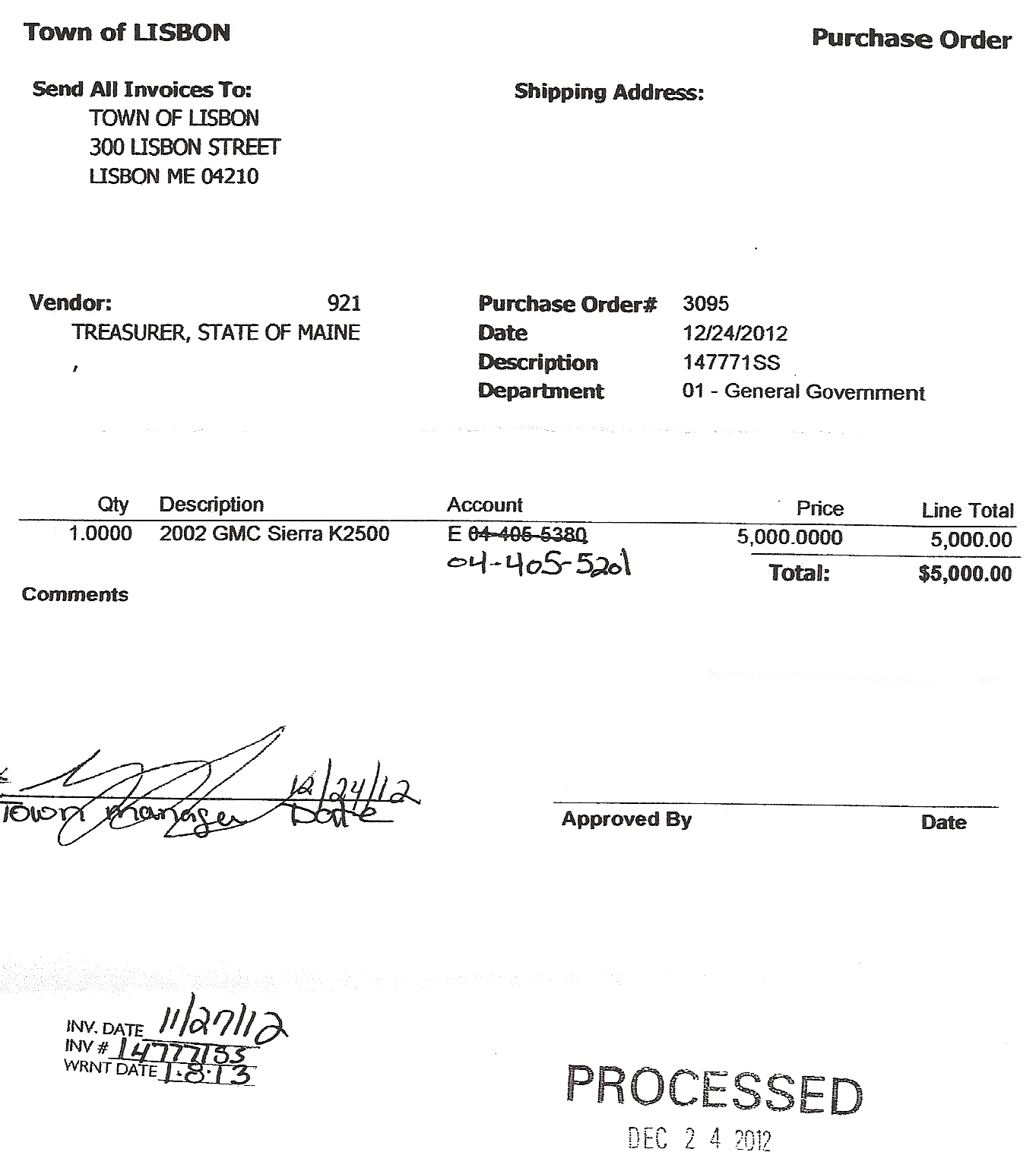

Second, was a 2002 GMC Sierra K2500 for $5,000.00 for the

Recreation Department? I have included a

copy of the Purchase Order but this line of accounting is crossed out and

another one added. This gets even

crazier because E04-405-5380, which was the original line of accounting, is for

Supplies Operating and this was changed to E04-405-5201 which is

Advertising/Notices. Trust me it

is a long stretch to justifying the purchase of a 2002 GMC Sierra K2500 under

Advertising/Notices. Also note there is

not sufficient funds in the Advertising/Notices account to cover the $5,000.00.

Both of these

Purchase Orders are signed by our town manager, Stephen

Eldridge; so much for verifying the information pertaining to our tax dollars. If you are wondering how this applies to

creating a slush fund. This is how the

town manager and the town council scam the taxpayers. First you increase each line item in the budget

under the pretense of needing to have a little more to cover emergencies when

in fact it is used to create the slush fund.

This is one of the reasons why the town raised our taxes last year.

Now think about this!

Each of the lines of accounting are going to show payment for these

trucks as expenditures under these line item so with this coming budget we will

have to increase these lines of accounting to cover the increase in

spending. These expenditures have absolutely nothing to do with these line

items but they are going to show up as money spent on these line items. This will increase our budget in the coming

year. This is how you create a

slush fund to be used by the town manager to purchase whatever he wants at

taxpayers’ expense.

How can you determine how much you need to operate if you

continue to apply unrelated items to line items? It is

impossible to determine where to make cuts in a budget if the accounting is not

posted to the correct line of accounting.

I now have shown where the furniture for the Communication Center was

charged to the wrong accounts and again with these two trucks.

This is what I have discovered on my own but it certainly

reveals a pattern of misappropriation of town funds.

Larry Fillmore

Concerned Citizen

No comments:

Post a Comment